Table of Contents

![]()

- 1. 10 Multi-Entity Accounting Automation Tips

- 2. Fast close accounting: How to close your books in 3 days or less

-

3. Intercompany reconciliation: 7 steps for accurate financial reporting

- What is intercompany reconciliation?

- Step-by-step intercompany reconciliation process

- 5 Common intercompany reconciliation examples

- 7 Key challenges in intercompany reconciliation

- How to do intercompany reconciliation in Excel

- Using Coefficient for seamless intercompany reconciliation

- Streamline your intercompany reconciliation

- FAQs

- 4. Strategic Scenario Planning: A Practical Guide for Finance Teams

- 5. Incremental Budgeting: A Complete Guide for Finance Teams

- 6. FP&A AI: Complete Guide to Artificial Intelligence in Financial Planning

- 7. Strategic budgeting: A complete guide to aligning finances with long-term goals

- 8. How to Create an Operating Budget (Step-by-Step Guide)

- 9. How to Do Vertical Analysis of a Balance Sheet

- 10. How to Do Sensitivity Analysis in Excel: A Complete Guide

- 11. CFO Reports to the Board of Directors: A Complete Guide

- 12. Cost volume profit analysis: A complete guide for finance teams

- 13. Workflow Automation for Fractional CFOs & Finance Service Firms

- 14. 11 Account Reconciliation Best Practices

- 15. How to build budget vs. actual reporting in spreadsheets

- 16. Automate Your Month End Close Process: A CFO’s 5-Step Playbook

- 17. 8 Must Automate Processes for Fractional CFO & Accounting firms

- 18. 6 Ways for CFO Firms to Provide Better Client Reporting

- 19. 6 Great Excel Report Templates for Fractional CFOs

- 20. How to Perform Price‑Volume‑Mix (PVM) Analysis in Excel — Free Template

- 21. How to Build a 13‑Week Cash‑Flow Forecast in Excel (Free Template)

- 22. How to Calculate Trailing‑12‑Month (TTM) Metrics in Spreadsheets + Free Template

- 23. How to do Scenario Analysis in Spreadsheets

- 24. Best Practices for Consolidating Financial Statements

Multi-entity organizations face a constant challenge. Transactions between subsidiaries create a web of accounts that must align perfectly. Without proper intercompany reconciliation, companies risk audit failures, compliance issues, and financial misstatements. Manual processes take 7-10 days for month-end close, creating bottlenecks that delay decisions.

This guide walks you through the seven-step reconciliation process. You’ll learn common examples, key challenges, Excel techniques, and automation strategies that speed up your close.

What is intercompany reconciliation?

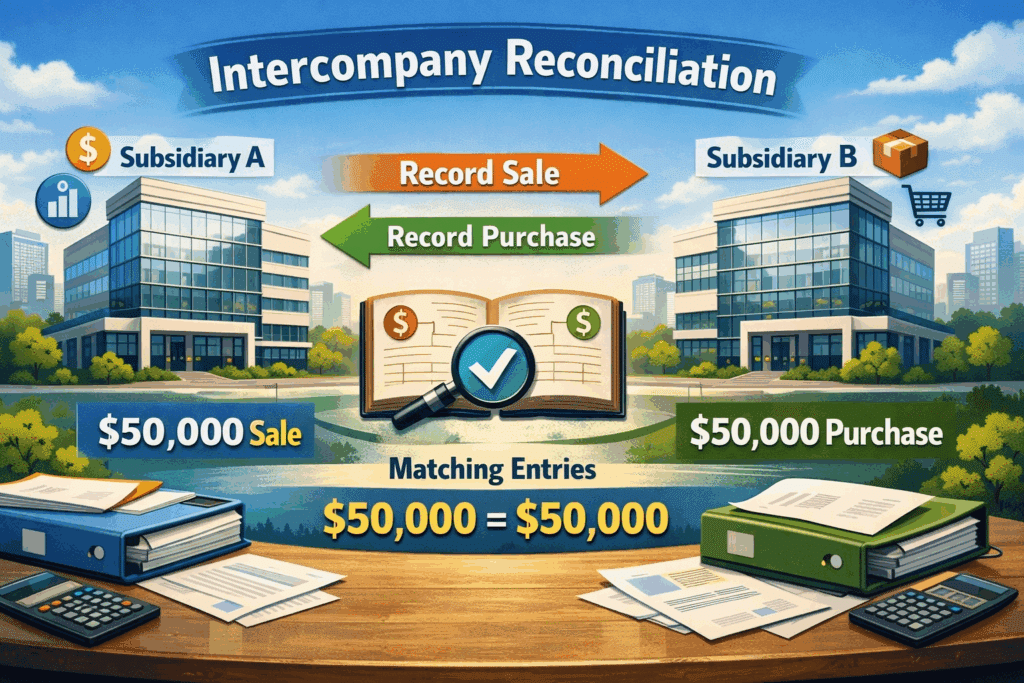

Intercompany reconciliation matches and verifies transactions between entities within the same corporate group. Each transaction one entity records should have a corresponding entry in the counterparty’s books. When Subsidiary A books a $50,000 sale, Subsidiary B should show a $50,000 purchase. These mirror entries must align for accurate consolidated reporting.

The process covers several account types:

- Due to/due from accounts track balances between entities

- Intercompany receivables and payables record amounts owed

- Intercompany sales and purchases capture revenue transactions

- Intercompany loans document financing between subsidiaries

Each account type requires careful matching to ensure both sides of every transaction align.

Consolidated financial statements eliminate intercompany transactions to prevent double-counting. Without proper reconciliation, organizations report inflated revenue, overstated expenses, and inaccurate asset positions. US GAAP (ASC 810) mandates elimination of intercompany income on assets remaining within the consolidated group. IFRS (IFRS 10, IAS 27, IAS 28) requires elimination of all intercompany transactions and balances.

External auditors scrutinize intercompany balances during reviews. Discrepancies raise red flags and extend audit timelines. Poor documentation creates compliance risks and potential penalties. Organizations that reconcile effectively demonstrate control over their financial reporting and maintain credibility with investors, lenders, and regulators.

Step-by-step intercompany reconciliation process

Step 1: Collect transaction data

Gather detailed records from all entities. This includes invoices, purchase orders, payment records, journal entries, loan agreements, and supporting documentation like contracts and approval records. The goal is complete visibility into every transaction that crosses entity boundaries.

Standardized formats make comparison possible. Each entity should use consistent GL accounts—”Intercompany Accounts Receivable” and “Intercompany Sales”—across all subsidiaries. Without standardization, matching becomes difficult. Subsidiary A might record a management fee while Subsidiary B calls it allocated overhead.

Step 2: Match transactions

Pair each transaction with its corresponding record in the other entity. Use unique identifiers—invoice numbers, transaction IDs, reference codes—to establish connections. Verify that:

- Amounts match exactly (accounting for currency conversion)

- Transaction dates align (or timing differences are documented)

- Debits and credits offset correctly

When Subsidiary A records a debit to accounts receivable for $100,000, Subsidiary B should record a credit to accounts payable for the same amount. Automated matching tools handle high volumes efficiently, achieving 90% auto-match rates and reducing manual matching time by 75%.

Step 3: Identify discrepancies

Review mismatches systematically. Common discrepancy types include:

- Timing differences where entities record transactions in different periods

- Currency conversion issues from fluctuating exchange rates

- Recording errors like data entry mistakes or incorrect account codes

- Incomplete transactions where one entity records before the counterparty processes

Use variance reports to highlight mismatches and exception reporting for amounts exceeding materiality thresholds. These tools help finance teams catch issues quickly rather than discovering problems during year-end audits.

Step 4: Investigate and resolve differences

Establish formal communication channels between entities. Define clear escalation procedures so complex issues don’t stall the entire process. Determine root causes by reviewing source documents, consulting entity controllers, and analyzing transaction history.

Resolution actions vary by issue type. Correct data entry errors in the originating system. Post adjusting journal entries to align records. Reclassify transactions to proper accounts when coding errors occurred. Document timing differences for future reconciliation periods.

Step 5: Post adjustments

Record corrections in both entities’ books simultaneously. Each adjusting entry should reference the original transaction, explain the reason for adjustment, identify who authorized the change, and link to supporting documentation.

Proper approval workflows ensure accuracy. Adjusting entries typically require controller or finance director approval, especially for material amounts. Post entries in the appropriate period based on when the original transaction occurred.

Step 6: Verify final balances

Confirm that all intercompany accounts balance to zero after adjustments. Due to/due from accounts should net to zero across all entities. Intercompany sales should equal intercompany purchases. All transactions should have corresponding offsetting entries.

Generate reconciliation reports showing opening balances, transactions during the period, adjustments made, and ending balances. Have someone other than the preparer review results—this separation of duties is a fundamental internal control auditors expect.

Step 7: Document and report

Create comprehensive documentation for audit purposes: transaction listings from both entities, variance reports, investigation notes, copies of adjusting entries, approvals, and reconciliation summaries.

Report results to management promptly. Key stakeholders need visibility into reconciliation status, outstanding issues, trends in discrepancy types, and time required to complete. Archive documentation according to retention policies—most organizations retain records for 7-10 years.

5 Common intercompany reconciliation examples

#1 Intercompany sales transaction

Subsidiary A sells goods worth $10,000 to Subsidiary B with cost of goods sold of $6,000. Subsidiary A debits Accounts Receivable and credits Sales Revenue for $10,000. Subsidiary B debits Inventory and credits Accounts Payable for the same amount. During consolidation, both entries must be eliminated to prevent double-counting revenue. Any unrealized profit in unsold inventory also requires elimination.

#2 Intercompany loan

Parent Company lends $500,000 to Subsidiary C at 5% annual interest. Parent records a note receivable and accrues interest income quarterly. Subsidiary C records a note payable and interest expense on the same schedule. Reconciliation verifies principal balances match and interest calculations align between both entities. Any differences in accrual timing or calculation methodology require investigation.

#3 Shared service charges

Corporate headquarters allocates $25,000 in IT costs to three subsidiaries based on headcount. Corporate records intercompany revenue for the full amount. Each subsidiary records its allocated share as an expense—$12,000, $8,000, and $5,000 respectively. Reconciliation confirms the total charges equal the total allocations. Allocation methodology must be documented and applied consistently each period.

#4 Currency conversion discrepancy

Subsidiary D in Europe invoices Subsidiary E in the US for €50,000. Subsidiary D records the amount in euros at the transaction date. Subsidiary E converts to dollars using a different exchange rate—perhaps month-end versus transaction date. The $2,300 variance requires investigation to determine which rate applies per company policy and whether an adjustment is needed to align both records.

#5 Timing difference

Subsidiary F ships goods on March 30 and records the sale in March following revenue recognition rules. Subsidiary G receives the shipment on April 2 and records the purchase in April per their receiving policy. Month-end reconciliation shows a temporary mismatch. This variance resolves in the following period once both entries are recorded, but requires documentation to explain the discrepancy to auditors.

7 Key challenges in intercompany reconciliation

#1 High transaction volumes

Large organizations process thousands of intercompany transactions monthly. Manual reconciliation becomes impractical at scale. High volumes increase error probability, delay issue detection, and create bottlenecks during close periods. Companies with 10 subsidiaries face 45 unique intercompany relationships to reconcile. Add more entities and combinations explode. Organizations need scalable processes that handle growth without proportional increases in staff or time. Automated matching tools that achieve high auto-match rates free analysts to focus on exceptions.

#2 Lack of standardization

Different entities often use inconsistent accounting policies, varying chart of accounts structures, and different transaction coding conventions. What one subsidiary calls “management fees” might be “allocated overhead” in another’s books. This makes matching exponentially harder. Implementing unified chart of accounts, consistent transaction codes, and synchronized accounting periods dramatically reduces reconciliation complexity. The upfront work of standardization saves countless hours during every subsequent close cycle.

#3 Timing differences

Timing misalignments arise when entities close books on different schedules. Different subsidiaries may record transactions at different times due to differing cut-off policies, invoice delays, or misaligned fiscal calendars. This creates temporary variances requiring investigation and complicates month-end close. Standardized close schedules help—when all entities close on the same day using the same cut-off rules, timing differences decrease significantly. Some organizations implement “soft closes” where preliminary balances reconcile before final close.

#4 Currency conversions

International organizations face exchange rate complexity. The same transaction may be recorded in different currencies. Exchange rates fluctuate between transaction date and payment date, creating realized and unrealized gains or losses. Entities may use different rates (spot, average, month-end). Currency rounding creates small differences that compound across many transactions. Establish clear currency policies defining which rates to use, specify rounding conventions, and document methodology comprehensively. Consistency matters more than which specific approach you choose.

#5 Communication gaps

Poor coordination between entities creates unnecessary friction. Delayed responses to inquiries, unclear escalation procedures, and insufficient collaboration tools all extend reconciliation timelines. When entity controllers are in different time zones, simple questions take days to resolve instead of hours. Shared workspaces where teams post questions and resolutions, scheduled reconciliation meetings with all entity representatives, and centralized documentation repositories improve coordination. Treating reconciliation as collaborative rather than isolated accelerates resolution.

#6 Manual processes

Spreadsheet-based reconciliation is labor-intensive and error-prone. Manual data extraction from multiple systems, copying between files, VLOOKUP formulas that break, and manual matching all create opportunities for mistakes. A single misplaced decimal point can create hours of investigation. Finance teams spend days collecting data instead of analyzing results. Manual processes don’t scale—as transaction volumes increase, reconciliation time grows proportionally without automation. This becomes a strategic constraint on growth and acquisition activity.

#7 Inadequate documentation

Poor documentation creates audit problems. Missing support for adjusting entries makes defense difficult. Unclear variance explanations frustrate auditors. No trail showing approvals raises control concerns. Insufficient detail for historical research when similar issues recur compounds the problem. Organizations that shortcut documentation pay the price during audits or when investigating future discrepancies. Comprehensive documentation should tell the complete story of how accounts were reconciled and why specific decisions were made.

How to do intercompany reconciliation in Excel

1. Set up separate sheets for each entity

Create a workbook with dedicated tabs for each subsidiary’s transaction data. Use consistent column structures across all sheets—transaction ID, date, description, account code, debit, credit, currency. This standardization makes cross-entity comparison possible. Include a master summary sheet that pulls totals from each entity tab for a consolidated view of intercompany positions. Name tabs clearly (Entity_A_Transactions, Entity_B_Transactions) so navigation stays simple as the workbook grows.

2. Use matching formulas like VLOOKUP, INDEX-MATCH

Excel formulas automate transaction matching between entities. VLOOKUP matches based on unique identifiers:

=VLOOKUP(A2, EntityB!A:D, 3, FALSE)

This looks up the value in A2 within Entity B’s data and returns the corresponding amount from column 3. The FALSE parameter ensures exact matches only. INDEX-MATCH provides more flexibility for large datasets or when match columns aren’t in the first position:

=INDEX(EntityB!C:C, MATCH(A2, EntityB!A:A, 0))

These formulas require clean, standardized data with unique transaction identifiers to work reliably. When identifiers aren’t unique or formatting differs between entities, formulas may miss matches or create false positives.

3. Build variance reports

Create reports showing differences between entities. Calculate variances with simple formulas: =EntityA_Balance – EntityB_Balance. Use conditional formatting to highlight significant differences—green for matched transactions, yellow for small variances within tolerance, red for material differences requiring investigation. Include transaction details from both entities, calculated variance amounts, percentage variance for context, and status indicators (matched, investigating, resolved).

4. Document adjustments

Maintain adjustment logs tracking every correction. Record the original variance amount, root cause identified, correcting entry details, responsible party, approval obtained, and date resolved. This audit trail proves essential when auditors request validation of your reconciliation procedures. Link each adjustment to supporting documentation stored in a central location. Keep the log current throughout the reconciliation process rather than documenting after the fact.

Using Coefficient for seamless intercompany reconciliation

Centralized data collection

Coefficient connects multiple ERPs and accounting systems directly to Excel or Google Sheets, consolidating intercompany data automatically. Coefficient supports 100+ systems including NetSuite, QuickBooks, Xero, Sage Intacct, and major data warehouses. Connect unlimited instances under a single account for consolidated reporting across all subsidiaries.

For NetSuite multi-subsidiary environments, OAuth configuration supports multiple subsidiaries and departments within a single connection. If your role includes cross-subsidiary access, import data from multiple subsidiaries through one connection. Use Records & Lists or SuiteQL queries to pull raw data, then build custom consolidation reports without NetSuite’s rigid formatting limitations.

This approach transforms consolidation into a review process rather than a data collection exercise. Finance teams spend time analyzing variances instead of wrestling with exports and imports.

Real-time monitoring

Schedule automated refreshes tracking intercompany balances throughout the month, catching discrepancies early rather than discovering issues at month-end. Configure hourly, daily, or custom refresh schedules based on business needs.

Real-time data enables proactive identification of mismatches before they compound. Finance teams can address timing differences, currency conversion issues, and recording errors as they occur. This continuous approach:

- Reduces month-end close time by 30%

- Identifies discrepancies throughout the period instead of scrambling at month-end

- Eliminates manual data entry errors through direct system connections

- Improves collaboration by sharing live reconciliation reports with entity controllers

Cyrq Energy, managing multiple geothermal plants, rebuilt months of NetSuite reporting work in days using Coefficient. They eliminated manual exports and saved over $50,000 annually while cutting several hours from weekly reporting workload.

Streamline your intercompany reconciliation

Intercompany reconciliation ensures accurate consolidated financial statements and regulatory compliance. The seven-step process provides a systematic approach: collect data, match transactions, identify discrepancies, investigate differences, post adjustments, verify balances, and document results. Common challenges—high volumes, lack of standardization, timing differences, currency conversions—require both process discipline and the right tools.

Excel works when enhanced with proper formulas and variance reports, but manual processes limit scalability. Automation delivers 70-90% time reduction and 50-80% fewer errors. Start by assessing your current process and identifying pain points. Even small improvements like standardizing chart of accounts yield significant benefits. Get started with Coefficient to transform intercompany reconciliation from a time-consuming bottleneck into a streamlined, automated process.

FAQs

What is a matching method for intercompany reconciliation?

A matching method defines criteria for comparing and aligning transactions between entities. Methods include automated rules based on transaction IDs and dates, VLOOKUP and INDEX-MATCH formulas in Excel, and AI-powered algorithms in specialized software. Effective matching methods establish clear criteria for when transactions match, set materiality thresholds for acceptable variances, and define escalation procedures for exceptions requiring manual review.

What is an intercompany reconciliation example?

Subsidiary A sells goods worth $10,000 to Subsidiary B. Subsidiary A debits Accounts Receivable and credits Sales Revenue. Subsidiary B debits Inventory and credits Accounts Payable for $10,000. During reconciliation, finance teams verify these amounts match and investigate any discrepancies. During consolidation, both the revenue and purchase must be eliminated to prevent double-counting in group financial results.

How to improve intercompany reconciliation?

Standardize processes across all entities using consistent chart of accounts and transaction codes. Automate matching with software that handles high volumes efficiently. Reconcile monthly instead of year-end to catch issues early. Use consistent currency rates and document exchange rate methodology. Establish clear communication channels between entity controllers. Maintain thorough documentation. Set materiality thresholds to focus on significant variances.

Why is intercompany reconciliation required?

Intercompany reconciliation ensures accurate consolidated financial statements that eliminate double-counting of revenue, expenses, assets, and liabilities. Compliance with GAAP (ASC 810) and IFRS (IFRS 10, IAS 27, IAS 28) mandates elimination of all intercompany transactions and balances. The process creates audit trails and demonstrates control over financial reporting. Without proper reconciliation, organizations risk audit failures, regulatory penalties, and inaccurate financial statements.